NEC — If we recreate the Dotcom bubble, we’ll do it right this time

A dinosaur in the world of business — evolving like a chicken but this chicken might just take flight

Back at it again with a good old Japanese stock that we think offers real value. This one is a tougher nut to crack—there is barely any coverage, and what little exists might as well be in Japanese. But do not worry dear peasant! Thanks to the combined power of AI capex—enough to build a nation with infrastructure rivaling Denmark—we can finally translate those ancient kanji into shareholder value.

Many thanks to Blue Owl Capital and the Magnificent 7—you really have changed the world for the better. Next up, maybe we can translate German civil servant jargon into actual German - AGI might not be so far as we might think!

We recently added also Nintendo and Mercari - we do reports on those later but as of now let us focus on NEC - the utilsation of Nintendo and Mercari may take longer anyway but with that we are pretty much set with our Japanese discoverage.

Overview

So what is the actual case with NEC ( 6701:TYO) ? Well it is one of Japan’s oldest and largest technology conglomerates, building everything from biometric identity systems and submarine cables to satellite components and enterprise AI platforms. For most of its 126-year history, NEC was a sprawling industrial-era giant that struggled to convert scale into margins. That story has been changing — and the market has been pricing that change, aggressively, for about five years.

Then it stopped.

Over the last year, NEC has significantly underperformed. The stock peaked at ¥6,194 in its 52-week range and is now trading around ¥4,065 — a drawdown of roughly 34% from those levels. This happened despite the company posting its best financial results in its history, with FY2026 (ended March 2026) delivering record operating margins, record free cash flow, and a dividend increase. The disconnect between fundamentals and price is where this thesis starts.

The consensus still sees ~48% upside from current levels, with 12 analysts all rating the stock a Buy and an average 12-month target of ¥6,008. That alone makes for a reasonable setup. But we think the consensus is still too conservative, because it hasn’t yet fully priced in the most structurally important development: NEC is quietly becoming Japan’s AI infrastructure backbone, and the monetisation of that position is still years away from showing up in reported earnings.

The Market is sassy recently

The market’s concern is legitimate on the surface. NEC’s FY2027 revenue guidance came in at ¥3,500 billion — a 2.3% decline year-over-year. The culprit is the peak-out of public sector IT projects in Japan. The wave of large government digitisation mandates — municipal system standardisation, fire and disaster prevention infrastructure — is cresting. Order volumes in this segment will flatten.

On earnings day (April 28, 2026), despite posting a 27.6% increase in Non-GAAP operating profit to ¥397.2 billion and achieving double-digit margins for the first time in its history, the stock fell nearly 4% and has been falling ever since.

The market sold the revenue guidance and ignored everything else, this has been the story about any tech stock recently - like we saw with PLAB 0.00%↑ or AVGO 0.00%↑ - their revenues just lag behind but they will spike eventually - capex is not slowing down.

NEC at ¥4,065 is a company trading on near-term revenue optics while undergoing what may prove to be the most significant margin and platform transformation in its history. The consensus already sees ~48% upside and every analyst covering it is a buyer. We think that consensus is still conservative, because it hasn’t modelled what NEC looks like in 2029-2030 if BluStellar’s AI ambitions are even half-delivered.

The AI investment cycle so far has rewarded the hardware layer — chip designers, high-bandwidth memory suppliers, data centre buildout or even grid and energy — with remarkable speed and consistency. The application and services layer, where AI-generated value is ultimately consumed by enterprises and governments, has been far slower to monetise and therefore far slower to be priced.

NEC sits almost entirely at the application layer. It builds the AI solutions that Japanese banks, manufacturers, hospitals, and local governments actually use. That is not the part of the AI stack that gets re-rated on every Nvidia earnings beat. That role isn’t valued by the market today, because the revenue from it hasn’t arrived yet. It will.

The next chapter belongs to the companies that take all that compute and actually connect it to the institutions that need it. NEC is one of the best-positioned companies in Asia to play that role — and the stock is still priced as if none of it is happening.

At ¥4,065, NEC trades at roughly:

17.5x forward earnings (FY2027 EPS estimate)

11.1x EV/EBITDA

~16x EV/FCF — against free cash flow that just grew 121% in one year

PEG of 0.89 — below 1, implying growth is underpriced relative to earnings trajectory

The consensus 12-month price target of ¥6,008 implies ~48% upside, which is already substantial. But that target is built on near-term earnings forecasts that largely reflect a revenue plateau narrative. It does not model a scenario where BluStellar’s AI monetisation accelerates meaningfully. Our view is that the base case is already more than ample. The upside case — driven by AI monetisation timing — is not in the consensus at all.

The reasons this isn’t priced yet are structural, not accidental. Enterprise AI adoption in Japan is slow by global standards — a combination of regulatory caution, talent shortages, and institutional conservatism. Surveys consistently show Japanese organisations lag global peers in AI deployment confidence. That slowness, frustrating in the near term, is actually a feature of NEC’s moat: the company has the trusted relationships with Japanese government and enterprise that no foreign AI provider can replicate. When those institutions do move, they will move through NEC.

The revenue from this transformation will not show up cleanly in the next two quarters. That is precisely the lag — and precisely why the stock is not yet pricing it. The market discounts what it can measure. It tends to underweight platform transformations whose payoff is 3-5 years out, especially when the near-term financial narrative (public sector revenue peak) gives bears a simple story to tell.

The FY2030 BluStellar target of ¥1.3 trillion in revenue at 25% margins implies an operating profit contribution of ~¥325 billion from this segment alone — from a base where NEC’s total company OP is ¥420 billion today. That kind of earnings power uplift is not in the consensus price targets.

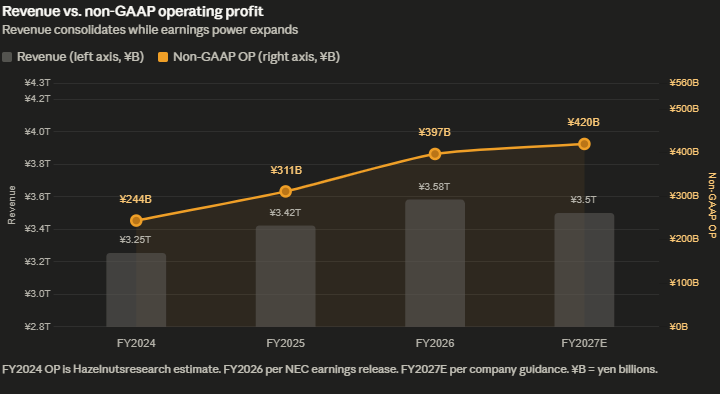

What the revenue decline narrative misses is that NEC is deliberately shedding low-margin work — it is exiting hardware resale, terminating unprofitable business PC sales, and winding down several legacy hardware contracts. On an adjusted, like-for-like basis, FY2026 revenue grew 9% year-over-year. The top-line “decline” in FY2027 is partially a deliberate quality upgrade of the revenue mix, not a demand problem.

Meanwhile, Non-GAAP operating profit is guided to grow another 5.7% to ¥420 billion in FY2027, implying a margin of ~12%. One year ago the company was operating at high single-digit margins. It’s now targeting 15.3% in domestic IT services alone by end of FY2027. The earnings power of the business is expanding even as total revenue consolidates. That dynamic tends to be systematically mispriced in the short run.

You either live with the Yen or die by it - no in-between

One of the most underrated aspects of NEC as a Japanese equity position is its domestic revenue concentration. Unlike Sony or Nintendo — where yen weakness is a structural tailwind and yen strength a material headwind — NEC derives the large majority of its revenue from Japan. Its business is rooted in domestic IT services, social infrastructure, and government contracts. Foreign exchange moves don’t carry the same directional risk.

In fact, a strengthening yen is constructively neutral-to-positive for NEC. It reduces the yen cost of imported components, supports the real purchasing power of NEC’s domestic corporate and government clients, and improves the JPY-translated value of international segment profits (primarily Avaloq in European wealth management and Netcracker in telecom software). As Japan’s central bank slowly normalises rates — with the yen recovering from multi-decade lows — NEC is one of the few large Japanese technology companies that doesn’t have to worry about a currency tailwind fading.

For investors who are cautious about Japanese equity exposure precisely because of FX risk, NEC offers a structurally different profile from the household names in the export-oriented space. It is pretty much our hedge to SONY 0.00%↑ is simple math.

Tail we win and head? We win again. The mahndi way or something like that - the book was not that memorable for us to look it up now. lol.

The blue crown jewel

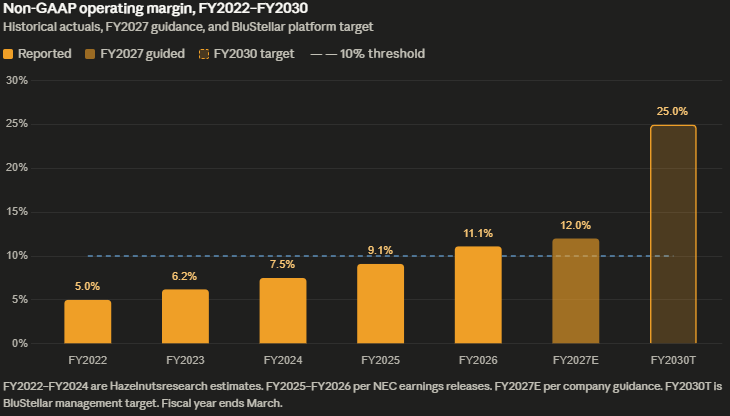

The single most important thing that happened at NEC in FY2026 was breaking through the 10% operating margin threshold. It sounds like a technicality, but for a company of NEC’s history and complexity, it represents a genuine inflection point in how the business operates.

This margin expansion is driven by BluStellar, NEC’s AI-native value creation platform launched as the centrepiece of its transformation strategy. BluStellar shifts NEC’s revenue mix from commoditised system integration and hardware toward high-value advisory, AI-driven automation, and outcome-based contracts. The fourth quarter of FY2026 showed what this can look like at scale: Q4 adjusted operating margins hit 15.6%, up 320 basis points year-over-year.

The long-term target for BluStellar is ambitious: ¥1.3 trillion in revenue by FY2030, with a 25% operating margin. For context, NEC’s total Non-GAAP operating profit guidance for FY2027 is ¥420 billion. If BluStellar executes even partially against that 2030 roadmap, the operating profit contribution from this segment alone could redefine what the company’s earnings look like.

Worth being honest about: the ¥1.3 trillion, 25% margin target is management aspiration, not formal guidance. We'd discount it significantly in any base case — say 50-60% execution — and the thesis still holds up. One underappreciated piece of the margin story that tends to get buried: the CSG Systems acquisition ($2.9 billion, completed early 2026) brings Netcracker's recurring telecom software revenue into the international segment. That is a structurally higher-margin business than legacy system integration, and the market hasn't fully digested what it adds to the earnings mix.

Free cash flow tells the same story. FCF grew 121.5% in FY2026 to ¥472.1 billion. That is an enormous cash generation machine being built underneath the “revenue is declining” headline. The company has also been returning capital aggressively — increasing its annual dividend to ¥38/share and running buyback programmes alongside it. The run up is justified but we think there might be room for more.

SpaceX but chill

NEC Space Technologies has manufactured over 9,500 satellite components for more than 400 spacecraft globally. Its work spans payload systems, power control units, attitude control hardware, data handling, and thermal management — the deep plumbing of space infrastructure.

Most recently (well it is actually not that recent), in January 2025, NEC (as prime contractor for JAXA’s LUCAS system) achieved the world’s fastest optical communication between a low-orbit Earth observation satellite and a geostationary relay satellite — 1.8 Gbps over roughly 40,000 km of space. In March 2026, NEC completed the payload design for a small technology demonstration satellite aimed at building Japan’s first optical communication satellite constellation, with an in-orbit launch scheduled for FY2027.

This matters for a few reasons. First, Japan is significantly ramping its defence and national security budget — targeting 2% of GDP by FY2028, roughly doubling from recent levels. NEC’s Aerospace and National Security (ANS) segment was one of the strongest contributors in FY2026 earnings, and the structural direction of Japanese defence spending is a durable tailwind. Second, satellite-based communications infrastructure is becoming increasingly strategic globally, and NEC is an established tier-one supplier in this ecosystem — not a newcomer trying to break in.

The space and defence exposure rarely gets a line in NEC’s equity narratives. It probably should because the whole Space-theme seems to stay rather than going away. From a political standpoint we think that East Asia will rather ramp production up than be happily watching from their chair as the West enters a new Space race - it’d be rather naive to assume that a nation like japan will stagnate for another 20 years, if change happens then now it is the time.

To put it into a Nutshell

NEC at ¥4,065 is a company trading on near-term revenue optics while undergoing what may prove to be the most significant margin and platform transformation in its history. The consensus already sees ~48% upside and every analyst covering it is a buyer. We think that consensus is still conservative, because it hasn’t modelled what NEC looks like in 2029-2030 if BluStellar’s AI ambitions are even half-delivered.

The AI investment cycle so far has rewarded the hardware layer — chip designers, high-bandwidth memory suppliers, data centre buildout or even grid and energy — with remarkable speed and consistency. The application and services layer, where AI-generated value is ultimately consumed by enterprises and governments, has been far slower to monetise and therefore far slower to be priced.

NEC sits almost entirely at the application layer. It builds the AI solutions that Japanese banks, manufacturers, hospitals, and local governments actually use. That is not the part of the AI stack that gets re-rated on every Nvidia earnings beat. That role isn’t valued by the market today, because the revenue from it hasn’t arrived yet. It will.

The next chapter belongs to the companies that take all that compute and actually connect it to the institutions that need it. NEC is one of the best-positioned companies in Asia to play that role — and the stock is still priced as if none of it is happening.

To be clear about what this is though: a 3-year hold, not a 12-month re-rating story. The AI opportunity is real but it will not show up in reported revenue this year or next. For the market to re-rate NEC on AI, it needs to actually see BluStellar revenue inflect in quarterly results — that is probably FY2028 at the earliest. The stock may drift from here before the catalysts arrive, and patience has a cost. Also worth monitoring: Fujitsu is fishing in exactly the same pond. It has nearly identical enterprise and government relationships, its own AI platform, and a Microsoft partnership. NEC’s Anthropic tie-up is a genuine differentiator, but the competitive dynamic is underexplored and deserves a closer look as the enterprise AI market develops but again, sources are scarce.

At ¥4,065, NEC trades at roughly:

17.5x forward earnings (FY2027 EPS estimate)

11.1x EV/EBITDA

~16x EV/FCF — against free cash flow that just grew 121% in one year

PEG of 0.89 — below 1, implying growth is underpriced relative to earnings trajectory

NEC’s current market cap sits at ¥5.4 trillion (~$37 billion) with 1.33 billion shares outstanding — mid-cap by global standards, which partly explains the coverage gap.

The consensus 12-month price target of ¥6,008 implies ~48% upside, which is already substantial. But that target is built on near-term earnings forecasts that largely reflect a revenue plateau narrative. It does not model a scenario where BluStellar’s AI monetisation accelerates meaningfully. Our view is that the base case is already more than ample. The upside case — driven by AI monetisation timing — is not in the consensus at all.

On a three-year view, the math runs like this. FY2027E EPS is ~¥233 at today’s 17.5x forward. Running margins from 12% today to ~15% by FY2029 on modest revenue growth gets to roughly ¥315 EPS. At 20x — a conservative re-rating as the margin story becomes consensus — that is a base case of ~¥6,300 (+55%). If AI revenue starts showing in quarterly results and the multiple re-rates to 24x, the bull case is closer to ¥9,000 (+120%). The bear — margins plateau early, no re-rating — still lands around ¥4,700 (+15%), which is not exciting but is not a disaster. For USD investors, yen strengthening from ¥145 to ¥130 stacks another ~12% on top of any equity return.

The consensus 12-month price target of ¥6,008 implies ~48% upside, which is already substantial. But that target is built on near-term earnings forecasts that largely reflect a revenue plateau narrative. It does not model a scenario where BluStellar’s AI monetisation accelerates meaningfully. Our view is that the base case is already more than ample. The upside case — driven by AI monetisation timing — is not in the consensus at all.NEC’s current market cap sits at ¥5.4 trillion (~$37 billion) with 1.33 billion shares outstanding — mid-cap by global standards, which partly explains the coverage gapNEC’s current market cap sits at ¥5.4 trillion (~$37 billion) with 1.33 billion shares outstanding — mid-cap by global standards, which partly explains the coverage gap

The reasons this isn’t priced yet are structural, not accidental. Enterprise AI adoption in Japan is slow by global standards — a combination of regulatory caution, talent shortages, and institutional conservatism. Surveys consistently show Japanese organisations lag global peers in AI deployment confidence. That slowness, frustrating in the near term, is actually a feature of NEC’s moat: the company has the trusted relationships with Japanese government and enterprise that no foreign AI provider can replicate. When those institutions do move, they will move through NEC.

The revenue from this transformation will not show up cleanly in the next two quarters. That is precisely the lag — and precisely why the stock is not yet pricing it. The market discounts what it can measure. It tends to underweight platform transformations whose payoff is 3-5 years out, especially when the near-term financial narrative (public sector revenue peak) gives bears a simple story to tell.

The FY2030 BluStellar target of ¥1.3 trillion in revenue at 25% margins implies an operating profit contribution of ~¥325 billion from this segment alone — from a base where NEC’s total company OP is ¥420 billion today. That kind of earnings power uplift is not in the consensus price targets.

The Risks — Briefly

Public sector plateau - The peak-out in government IT is real. If volumes contract faster than BluStellar fills the gap, the revenue shortfall could be worse than the guided -2.3%, and the market will react accordingly.

Fujitsu - They share NEC’s enterprise relationships, are building their own AI capabilities, and are bidding for the same domestic contracts. NEC’s Anthropic partnership is a differentiator, but not an impenetrable moat.

BluStellar execution - The FY2030 targets are aspirational. Partial delivery is the base case. If margins plateau in the mid-teens before reaching 25%, the re-rating stops there — still meaningful upside, but not the full thesis.

Patience has a cost - No visible near-term catalyst means the stock can drift sideways for 12-18 months. Know what you own.

Thanks for reading!

Do you think it will outperform or no? Vote below!

⸻

🌰 Hazelnuts Research – The search for quality at a fair price.

Not every price drop is a risk. Some are a gift – if you understand what you’re buying.

⸻

⚠️ Disclaimer

The information provided herein is for informational purposes only and also serves as a personal trading journal for the author. It represents the author’s personal analysis and opinion and does not constitute financial advice, investment recommendations, or an offer or solicitation to buy or sell any securities. The author is not a registered financial advisor, and readers should consult with their own financial advisors before making any investment decisions.

The content presented is based on publicly available information, sources believed to be reliable, and insights gathered through a combination of manual and automated analysis tools. While efforts are made to ensure accuracy, the author does not guarantee the completeness or timeliness of the information provided and assumes no responsibility or liability for any errors or omissions in the content or for any actions taken in reliance on the information presented.

Readers should be aware that investing involves risks, and past performance is not indicative of future results. The author may or may not hold positions in the companies mentioned. Any investment decisions made based on the information in this report are at the sole discretion of the reader, who assumes full responsibility for their own investment activities.