SIXT - Hidden Value in Germany

A 5-minute pitch: limited downside with significant upside.

Dear Valuable reader, we are trying to shorten our general thesis to focus on the important aspects - let us know if you liked it.

BTW -very important- if you have a SIXT share you can get up to 15-20% off when renting. Just Google to see if it applies for your region too.

WE MADE THE REPORT ABOUT THE COMMON STOCK BUT PREFER THE $SIX3 STOCK. Why? Because the Sixt family already holds ~58% of the voting rights, so your “vote” ( Literally lol) doesn’t really move the needle. With the $SIX3 (Preference Shares), you get the same business but with higher dividends and a cheaper entry price.

Anyways here we go: This is our attempt of a 5 minute pitch.

⸻

Company: SIXT.SE

Ticker Symbol: SIX2

Current Price: ~68.90€

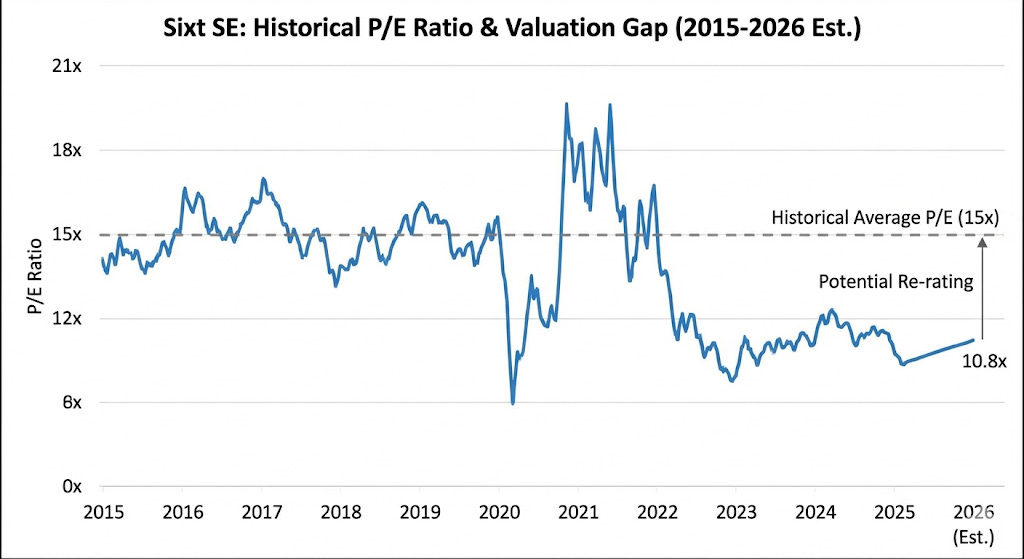

P/E (KGV): ~11.3x

⸻

1: The Summary – The Asymmetric Dislocation

Sixt SE ( $SIX2 ) is valued as a generic, commoditized rental company like its struggling US peers, Hertz and Avis.

While the broader industry struggles with post-pandemic normalization and “EV-related” fleet losses, Sixt stands alone as a quality Compounder.

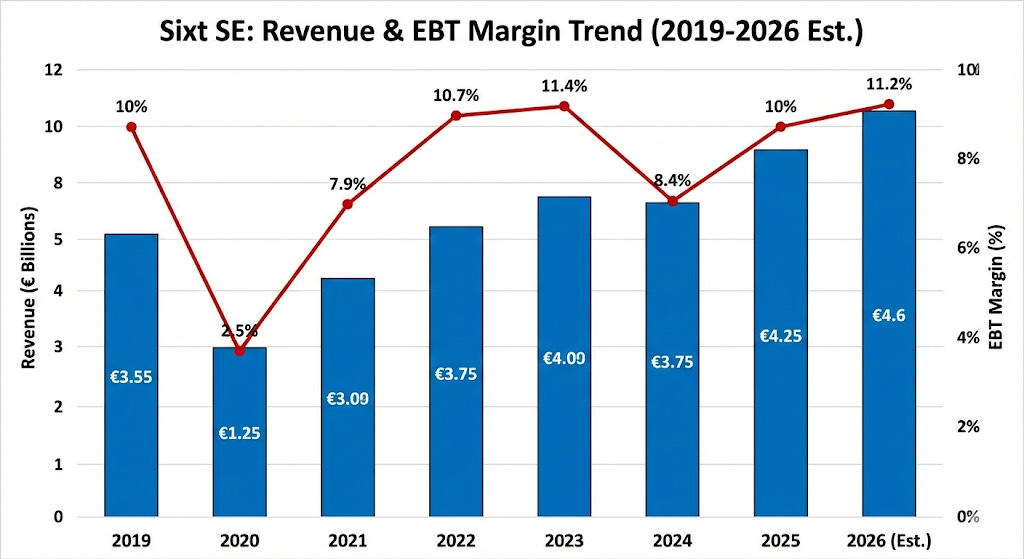

As of early 2026, the data is clear: Sixt has successfully navigated the high-interest-rate environment and used-car price volatility. With record revenues ( 4.25B) and a return to its target 10% profit margins, the current share price represents a significant discount to its intrinsic value. We believe Sixt offers a realistic, risk-adjusted path to double its market value within the next 3 to 4 years.

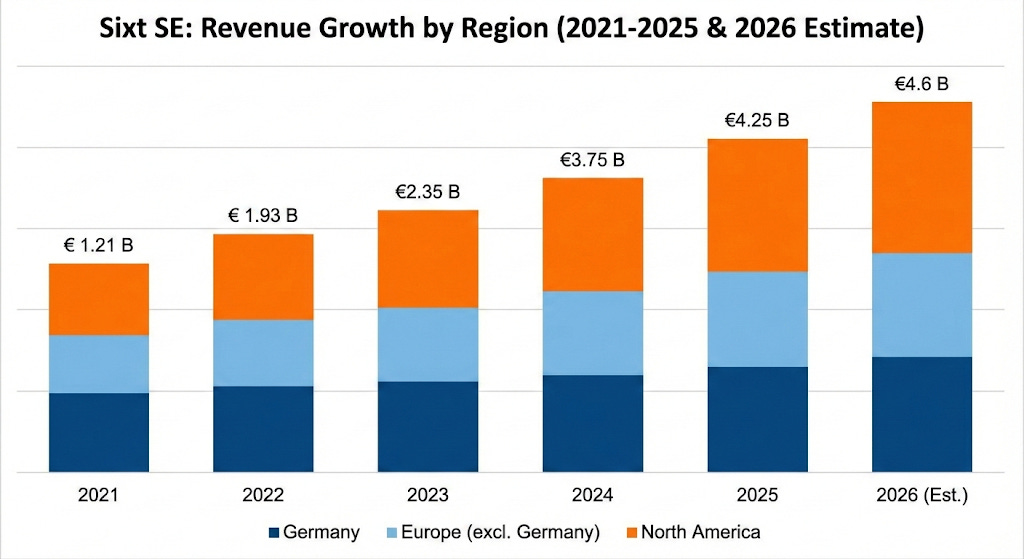

Here a quick overview how and where get their money as of right now:

• Europe (Excl. Germany): ~40% of Revenue. Massive expansion in Spain, France, and Italy.

• Germany: ~30% of Revenue. This is a Heimspiel, high-margin corporate revenue and a stable foundation. easy money.

• North America: ~30% of Revenue. Starting from 0% in 2011, this segment is now a massive third of the company and steadily growing.

• Rest of World: While Sixt is present in places like Dubai, Singapore, and Australia, these are primarily franchise models. They provide high-margin royalty fees but represent a smaller portion of the total Group revenue compared to the three pillars above. Still nice though since it’s low risk but profitable.

The EV strategy is simple, don’t buy TSLA 0.00%↑ since they’re not only expensive to buy but also expensive to maintain. They agreed to buy 100K cars from BYD, yeah the Chinese manufacturer. By using BYD, Sixt gets better price stability and “buyback” agreements that protect them from used-car market crashes. Pretty smart if you ask us.

2: The Pitch – Focus on luxury

Why does Sixt win where others fail? Well they didn’t reinvent the wheel but take a different approach :

• The Advantage: In Europe, roughly 80% of Sixt’s fleet is covered by “buyback agreements.” which we just mentioned above. This means manufacturers like BMW, BYD and Mercedes are contractually obligated to buy the cars back at a set price. If used car prices crash, the manufacturers bleed—not Sixt.

• The US Growth Engine: The US is the most profitable car rental market on earth. Sixt is becoming a major US challenger. By focusing on the top 50 airports and offering a premium experience (BMW/Audi for the price of a Ford), Sixt is aggressively taking market share from incumbents who are plagued by old fleets and poor service. They also upgrade you easily which leaves room for speculation ( gamble like behavior almost) from customer side. They aiming for 20% CAGR which is very optimistic but not totally out of reach.

• Variable Cost Mastery: Unlike airlines or hotels, Sixt’s costs are 70% variable. If a recession hits, they simply buy fewer cars. This flexibility allows them to remain profitable when others are fighting for survival.

They also tried recently a couple new programs like SIXT+. They are aggressively pushing SIXT+, a car subscription service that sits between a rental and a lease. Unlike a one-off rental, SIXT+ creates “sticky” customers who pay a monthly fee. It offers the convenience of a lease (new cars, maintenance included) but with the ability to cancel monthly. This could be a massive hit within “Asset-Light” mobility.

3: The Catalysts – What Will Drive the Re-Rating?

For an investment you need specific events to change the market’s mind. For Sixt, these are the three primary triggers we are watching:

1.

The market has been skeptical about Sixt’s 10% EBT (Earnings Before Tax) margin target. As upcoming 2025/2026 quarterly results confirm that these margins are stable and repeatable, the “discount for uncertainty” will vanish though we believe a lot of fear concerning tariffs (regarding German cars, since that’s what they focus on) and economic uncertainty is priced in.

2.

Currently, the US expansion is seen by some as a “cash burn” phase. When Sixt explicitly breaks out the profitability of its mature US hubs (like Miami and LAX), it will prove that the US isn’t just a growth story but a strategic play.

3; The Valuation

Sixt currently trades at roughly 11x earnings. Historically, when the market recognizes Sixt as a high-quality compounder, it trades closer to 15x.

The Calculation to €135:

• The Growth: If revenue grows by 9% annually and margins hold at 10.5%.

• The Multiple: If the P/E ratio moves from 11x back to its 15x average.

• The Result: A share price of approximately €135 by 2028, plus a consistent 4% annual dividend yield while you wait.

Our verdict: We will be accumulating $SIX2 (Preference Shares). The market is pricing in a “commodity” future for a company that is delivering “premium” results.

Biggest risk? Moat.

We are not talking about ASML here, in the rental car business customers usually choose the cheapest car, there is no brand loyalty or anything even resembling that. Basically what we’re saying is that if they can’t keep up with competitive pricing they get pushed away faster then they entered the market.

Thanks for reading!

⸻

🌰 Hazelnuts Research – The search for quality at a fair price.

Not every price drop is a risk. Some are a gift – if you understand what you’re buying.

⸻

⚠️ Disclaimer

The information provided herein is for informational purposes only and also serves as a personal trading journal for the author. It represents the author’s personal analysis and opinion and does not constitute financial advice, investment recommendations, or an offer or solicitation to buy or sell any securities. The author is not a registered financial advisor, and readers should consult with their own financial advisors before making any investment decisions.

The content presented is based on publicly available information, sources believed to be reliable, and insights gathered through a combination of manual and automated analysis tools. While efforts are made to ensure accuracy, the author does not guarantee the completeness or timeliness of the information provided and assumes no responsibility or liability for any errors or omissions in the content or for any actions taken in reliance on the information presented.

Readers should be aware that investing involves risks, and past performance is not indicative of future results. The author may or may not hold positions in the companies mentioned. Any investment decisions made based on the information in this report are at the sole discretion of the reader, who assumes full responsibility for their own investment activities.

Doesn't Sixt have the lowest ratings of all the major car rental services in the US? I always pass on them despite their low prices, because i've read too many bad reviews.

This is very interesting article! I wasn't aware of Sixt before. Now I know where to go next time I want a vacation car rental from airport.